For goods, the seller needs to print three copies. The original copy for the recipient, the duplicate copy for the transporter, and the triplicate copy for the supplier.

GST Tax Invoice, Rules & Procedure

Complete guide on GST Invoice, GST Invoice Rules, GST Bill formats, various types of GST Invoice, procedures & other important GST related information pieces.

In 2017, the Government of India introduced GST – Goods and Service Tax. It is a centralized tax levied by the federal government, and it replaces many indirect taxes like VAT, excise duty, services tax. Any business that exceeds the INR 40-Lakh turnover threshold needs to register under GST. However, businesses that operate in the North-East region of India or any other hilly region can register for GST if the turnover exceeds INR 10 Lakh.

If you are a business owner and want to learn more about the GST invoice rules, you may find this blog helpful.

What is a GST Invoice?

Before the GST came into being, a supplier or seller needed to generate various invoices for different taxes. For example, there were excise, tax, retail, and so on. After GST replaced other indirect taxes, businesses generated only one tax invoice under the GST invoice rules.

Now, any business that has a GST registration must furnish a tax invoice to the buyer containing the transaction details between the seller and buyer.

This information includes –

- Product name

- Description of product

- Quantity of goods or services sold

- Details of the supplier and the purchaser

- Terms of supply

- Date of supply

- Price of each good sold or service rendered

- Discount (if there is any)

Mandatory fields in GST Invoice (Prescribed GST Bill Format)

As per the GST invoice rules, a tax invoice must be fed data to its mandatory fields. One may find the below-mentioned information on a GST invoice –

- Date and Invoice number

- Name of Customer

- Billing Address and Shipping Address of customer

- GSTIN of Tax payer and Customer (if registered)

- Place of supply

- HSN Code (Harmonized System of Nomenclature Code) or SAC for goods and services

- Quantity, description or other relevant item measure/details

- Taxable value/applicable discount

- GST rates and total GST charged, including details of applicable CGST/SGST/IGST for the item

- Signature of the supplier

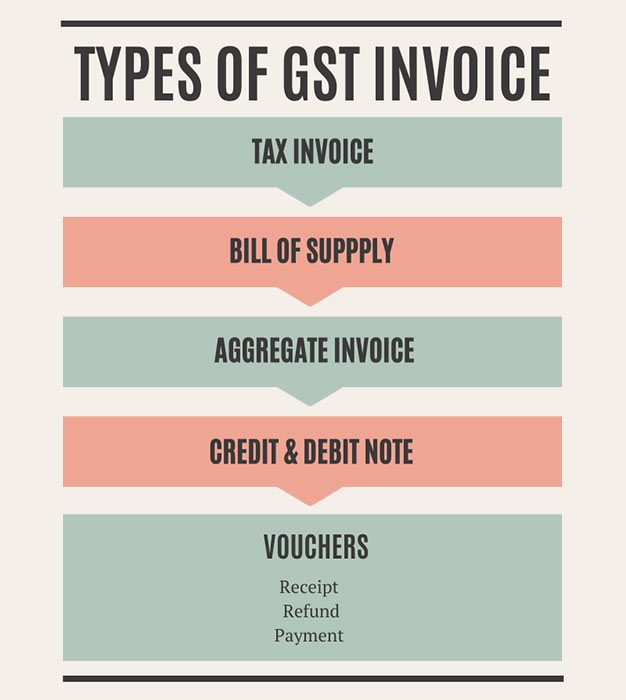

Types of GST Invoice

There are several types of GST invoices, and this classification is based on the GST invoice rules of India.

Tax Invoice –

Under GST invoice rules, any GST registered business owner supplying goods or services must issue Tax invoices to its buyer. It is commonly known as “Invoice” or “Tax Invoice”. Even though it is mandated to issue an invoice, the seller or supplier may not raise an invoice if the transaction amount is less than INR 200. If it is greater than the said number, the Tax Invoice needs to be issued within 30 days from the date of supply.

Bill of Supply –

Bill of Supply is a fairly new concept in the GST regime. Generally, a bill of supply does not contain any tax amount as the seller will not yet be able to charge GST. A bill of supply is issued under two circumstances –

- When a person is registered under GST composition scheme

- When the supply consists of exempted goods or services

Again, the issuance of bill of supply becomes optional if the transaction amount is below INR 200.

Aggregate Invoice –

Aggregate invoice replaces multiple tax invoices with an amount lower than INR 200. For example, the seller raises several invoices amounting to INR 30, INR 85, INR 186, INR 95. Now, the seller can issue an aggregate invoice of INR 396 to replace all the previous invoices. As per the GST invoice rules, an aggregate invoice can only be raised for an unregistered buyer.

Credit & Debit Note –

A seller issues a credit or debit note in case of a wrong GST invoicing. To explain, here is an example. Assume a seller sold a service or goods with 18% GST and raised an invoice amounting to INR 500. However, the product is categorized under 12% GST, and the original invoice should have been INR 470. In that case, the seller would raise a credit note of INR 30 for the vendor.

Debit is exactly the opposite. According to the GST invoice rules, the seller raises a debit note if he had mistakenly charged a lesser GST. Reversing the previous example, the seller had raised an invoice of INR 470 instead of the correct amount of INR 500. Now, he would have to raise a debit note amounting to INR 30 to the buyer.

Receipt, Refund, Payment Voucher –

When a GST registered seller person receives any advance from the buyer, the former needs to issue a receipt voucher acknowledging such payment. Now, imagine a scenario where a receipt voucher has been issued to the buyer, but the buyer received no supply. In that case, as per the GST invoice rules, the registered seller should issue the Refund Voucher.

The invoice rules under GST also clarify that when a registered buyer receives any supplies of goods or services from an unregistered seller, the buyer must issue a payment voucher to the supplier. The buyer should issue the voucher while making the payment under reverse charge. A payment voucher is issued under two circumstances –

- When a registered person under GST receives supplies from an unregistered person

- When a registered person makes supplies on which tax is payable under reverse charge mechanism

Who should issue GST Invoice?

Businesses that are GST registered issue GST Invoices. According to the invoicing rules under GST, the registered seller must maintain a specific GST invoice format. On the other hand, vendors registered with the GST council and have their own GSTIN or GST Identification Number, need to provide the bills of purchase in a particular GST invoice format.

GST Invoices under special cases

As per the invoicing rule under GST, the seller must furnish the invoice in a definitive GST bill format. However, there are certain exceptions or relaxations. It becomes difficult for businesses with offices in multiple cities to supply goods or services to claim the input tax credit.

For example, Company A is situated in Kolkata, but has branches in Bangalore, Gurgaon, and Mumbai. If the Gurgaon branch issues an invoice, the Kolkata branch cannot claim the input tax credit. In that case, Company A in Gurgaon would issue an ISD invoice instead of a regular tax invoice. However, to benefit from the relaxation, the Company must be registered as an ISD or Input Service Distributor.

If you want to know more about ISD, you can click here. You can also know how to claim input tax credit.

What are GST Invoice Rules

Here are the invoicing rules under GST –

For Goods,

- Invoicing under GST should be issued on or before the delivery date in normal case of goods

- For continuous supply of goods, invoicing under GST has to be issued on or before the day when the account statement is issued

For services,

- Invoicing under GST should be issued within 30 days of the supply being made in case of any general case of services

- For services associated with banks or NBFCs, invoicing under GST has to be issued within 45 days of the supply being made

Revising an already-issued tax invoice

Revising an already-issued GST invoice can be revised. In case of any mistakes in the GST invoice, the seller can rectify the errors, but the rectifications need to be reported in the monthly returns. There can be two types of revisions –

- Upward revision

- Downward revision

The seller can request for an upward revision with a supplementary invoice, whereas a downward revision can be done using a credit note to that effect. For a complete revision in the invoice, a “revised” invoice has to be issued. Supplementary invoices include debit or credit notes, depending on the nature of revision.

As we mentioned before, an upward revision or tax deficiency requires the registered seller to issue a debit note, and a downward revision or overcharged tax requires a debit note.

Ways to Personalize GST Invoices

Although there is a prescribed GST bill format per the invoicing rules under GST, one can personalize the prints using the business logo and design. However, mandatory fields should be maintained.

Explore our Buying Guides

FAQs

Have questions?