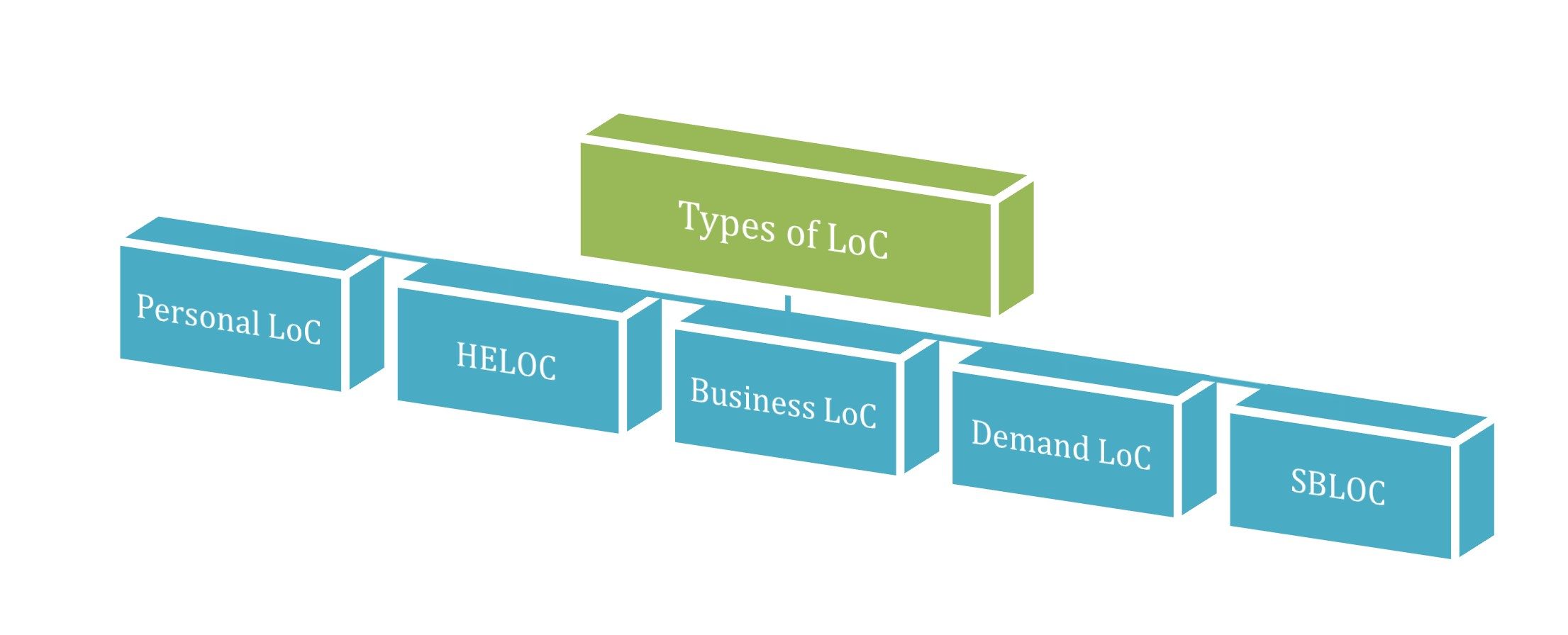

Personal Line of Credit

A personal Loc gives you access to money you can borrow, payback, and borrow again whenever you need it. This is an unsecured LOC; therefore, to open a personal LOC, it's important to have a good credit history without any missed payments. A 670 or higher credit score and a steady income are required for this line of credit India. While having savings or assets like stocks or CDs (Certificates of Deposits) can be helpful, they're not always necessary to get a personal LOC.

People use personal LOCs for different reasons. They can be handy in emergencies, for special events like weddings. To protect against overdrafts in bank accounts, for travel, and to manage irregular income. It's like having a financial safety net that you can rely on when you need extra money without having to go through a lengthy loan application process each time.

Home Equity Line of Credit (HELOC)

HELOC is a popular type of secured LOC. As the name suggests, the value of a home secures them. It also takes into account the outstanding mortgage balance. Therefore, the credit limit is usually set at around 75% to 80% of the home's market value minus the amount owed on the mortgage.

With this type of secured HELOC, there is a draw period that usually lasts around 10 years. During the said period, the borrower can access funds, repay them, and borrow again as needed. After the draw period, the remaining balance becomes due, which is paid either in a lump sum or through extended repayment options.

It's important to note that HELOCs often involve closing costs, such as appraisal fees, to assess the value of the property used as collateral. These costs are incurred during the initial setup of the HELOC.

Business Line of Credit

A business line of credit is a business credit taken as per business needs instead of taking a fixed loan. Before extending a line of credit for a business, the financial institution assesses factors such as market value, profitability, and risk. Based on this evaluation, the credit in business may be secured or unsecured. While the interest rate remains variable, it is reflective of the size of the requested LOC and the evaluation results.

Demand Line of Credit

A type of credit is not that common, and it can be secured or unsecured. Unlike traditional loans with predetermined terms, this on line credit facility does not have a specific maturity date or set repayment plan. With a demand LOC, the lender can require the amount borrowed to be paid back at any time.

The borrower can request funds from the credit line whenever required, up to a predetermined credit limit. The borrower only pays interest on the amount borrowed, and there is typically no penalty for repaying the borrowed funds early. Repayment can be interest-only or can include principal, based on the terms of the LOC.

Securities-Backed Line of Credit (SBLOC)

As the name suggests, SBLOC is a type of secured-demand LOC that uses the borrower's securities as collateral. With an SBLOC, investors can borrow a certain percentage (usually between 50% and 95%) of the value of their securities held in their accounts.

Unlike other types of loans, SBLOCs are considered non-purpose loans, which means the borrowed funds cannot be used to purchase or trade securities. However, they can be used for a wide range of other expenditures.

Borrowers of SBLOCs are usually required to make monthly interest-only payments until the loan is fully repaid or until the brokerage or bank calls for payment. If the value of the investor's portfolio declines and falls below the required level, the lender may demand immediate repayment of the loan.

SBLOCs provide investors with a convenient way to access funds without having to sell their securities. They offer flexibility in terms of borrowing amounts and can be used for various financial needs, such as covering personal expenses, making home improvements, or funding business ventures. However, it's important for borrowers to understand the terms and risks associated with SBLOCs, including potential margin calls and changes in the value of their securities.

What is an Amazon Business Line of Credit?

The Amazon Business Line of Credit is a financing option designed for businesses that regularly shop on Amazon Business or Amazon.com. It is managed by Synchrony Bank and offers convenient inventory management, and you can easily track purchases.

The list of conveniences doesn't end here. When you sign up for an Amazon Business Credit Line, you will receive personalized support from a dedicated account management team. They will assist you with account setup, customization, and ongoing account management.

If your business spends over $100,000 annually, an account specialist will be assigned specifically to your account. Enjoy priority service and top-notch support tailor-made for high-spending businesses.

Once the account is set up, you can create separate accounts for your organization's companies, locations, or departments. This enables you to receive easy-to-read monthly statements that provide transaction details and product-level information for each invoice.

The Amazon credit line operates as a pay-in-full credit, meaning there are no interest charges or annual fees. You have 55 days to make payment for all Amazon Business purchases, and the credit line must be paid off completely at the end of each payment term.

It's important to be aware that certain items cannot be purchased using the Amazon Business LoC. These items include cell phones, textbook rentals, e-documents, games, and software downloads, digital newspapers and magazine subscriptions, Prime memberships, recurring deliveries, and Subscribe & Save. Additionally, the credit line does not cover Amazon gift cards sent via email or available for print at home.

How can One Apply?

Let's dive into how you can apply for the Amazon Business line of credit.

First, visit the credit line page on Amazon Business website and click on the Apply Now button. You will find detailed information about the credit line and its features on the application page. Once you proceed with the application, you will be redirected to the application form provided by Synchrony Bank, the financial institution that partnered with Amazon for the credit line.

Then you need to fill out the application form with accurate and complete information.

The application form will require you to provide the following details:

➔ Your business name

➔ Business address, phone number, and email address

➔ Business Type

➔ Annual revenue

➔ Tax ID number

➔ Information about the authorized representative or owner of the business

While filling out the form, you will have the option to choose whether or not to provide a personal guarantee. The personal guarantee is not mandatory, but it may be required if your business is less than two years old or lacks an established credit history.

Review your application carefully to ensure all information is accurate.

How Is Amazon Business Able to Provide Credit?

Amazon Business is able to provide credit to customers through its Amazon Business American Express Card and Amazon Business Prime American Express Credit Card. The Amazon Business American Express Card offers customers the ability to earn rewards on purchases made at Amazon, while the Amazon Business Prime American Express Credit Card allows customers to earn 5% cash back on all purchases made at Amazon, Amazon Business, and AWS. Both cards also offer a 90-day interest-free period with no annual fee.

In addition to these two cards, customers can also apply for an Amazon Credit Line, which provides access to a line of credit that can be used for business purchases. Customers can manage their line of credit online via Synchrony Bank and make payments either online or by mail. Overall, Amazon Business provides a range of options for customers looking for credit solutions that are tailored to their needs.

Features Of Amazon Business Line of Credit Solution

Here are some of the key features of Amazon Business line of credit: